What is the North America Low Speed Vehicle Market Overview – definition, scope, and significance?

The North America Low Speed Vehicle (LSV) market comprises vehicles designed to travel at 25 mph (40 km/h) or less, primarily for short‑distance transportation in controlled environments such as campuses, resorts, industrial parks, and municipal zones. The scope covers four vehicle types—Commercial Turf Utility Vehicles, Golf Carts, Industrial Utility Vehicles, and Personnel Carriers—powered by diesel, electric, or gasoline propulsion. This segment is significant because it supports sustainable mobility, reduces fuel consumption, and meets regulatory incentives for low‑emission transportation across diverse North American applications.

What are the market drivers, restraints, challenges, and opportunities shaping the North America Low Speed Vehicle market?

Key drivers include rising demand for eco‑friendly transport, increasing investment in campus and industrial infrastructure, and supportive legislation that encourages electric LSV adoption. Restraints stem from stringent safety standards, limited top speed restricting broader usage, and higher upfront costs for electric models. Challenges involve supply‑chain volatility for battery components and the need for specialized maintenance networks. Opportunities arise from the expanding e‑mobility ecosystem, integration with smart‑city platforms, and potential for autonomous LSVs in logistics and hospitality.

What are the current growth trends in the North America Low Speed Vehicle market?

Current trends highlight a rapid shift toward electric propulsion, driven by declining battery costs and corporate sustainability goals. Manufacturers are introducing modular designs that allow quick conversion between utility and passenger configurations. Telematics and IoT connectivity are being embedded for fleet management, route optimization, and predictive maintenance. Moreover, a niche but growing interest in autonomous low‑speed shuttles is emerging in closed‑site environments such as university campuses and large resorts.

How did COVID‑19 impact the North America Low Speed Vehicle market and what is the recovery trajectory?

The pandemic caused a temporary dip in demand as campuses, hotels, and golf courses closed, leading to delayed orders and decreased fleet expansions. However, post‑2021 recovery accelerated as institutions reopened and prioritized contact‑less transportation solutions. Health‑focused redesigns—such as enhanced ventilation and touch‑free charging—stimulated renewed purchases. The market is now on a steady upward trajectory, supported by heightened hygiene awareness and the resurgence of recreational and industrial activities.

Who are the major competitors and what is the level of consolidation in the North America Low Speed Vehicle market?

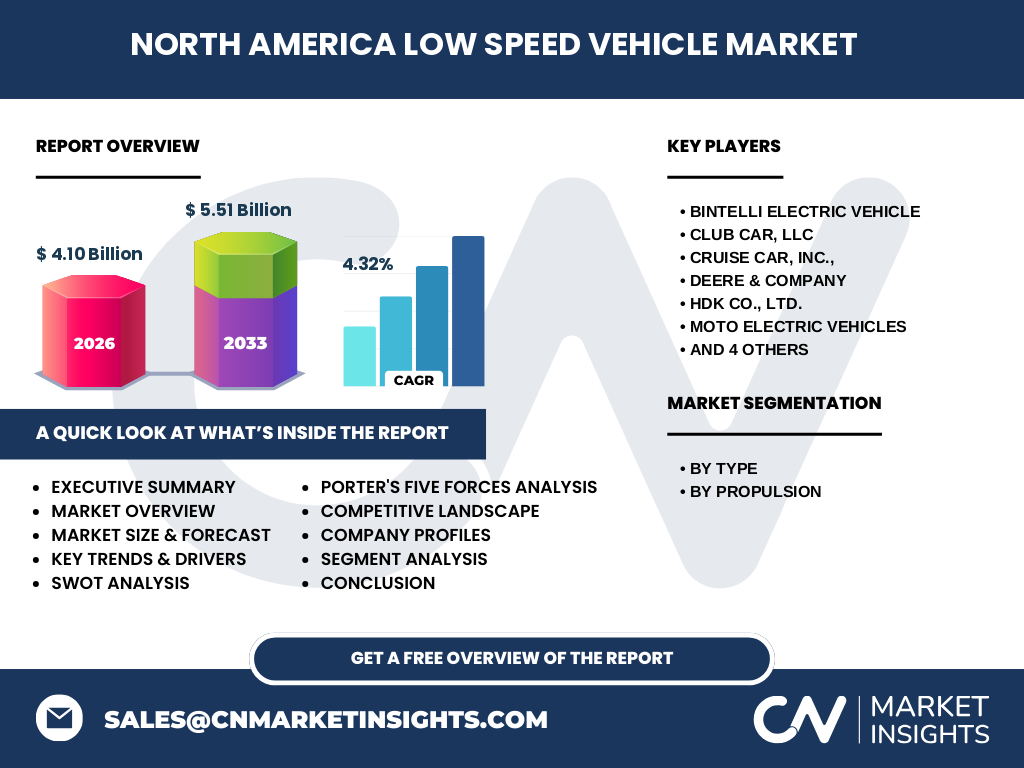

The competitive landscape features established OEMs and emerging electric specialists. Prominent players include Bintelli Electric Vehicle, Club Car, LLC, Cruise Car, Inc., Deere & Company, HDK Co., Ltd., Moto Electric Vehicles, Polaris Inc., Textron Specialized Vehicles Inc., The Toro Company, and Yamaha Golf‑Car Company. While the market remains fragmented, recent strategic alliances and joint ventures—especially in battery technology and telematics—signal early stages of consolidation, positioning leading firms for scalable growth.

What does the executive summary reveal about the North America Low Speed Vehicle market?

The executive summary underscores a $4.10 billion market size in 2026, projected to reach $5.51 billion by 2033, reflecting a 4.32 % CAGR. Growth is propelled by electrification, regulatory support, and expanding use‑cases across commercial, recreational, and industrial domains. Competitive dynamics are shifting toward technology‑focused players, and the market’s resilience post‑COVID‑19 demonstrates strong demand fundamentals. Stakeholders are advised to invest in electric platforms, data analytics, and strategic partnerships to capture emerging value.

What are the market forecast expectations for 2025‑2032?

Based on the provided CAGR of 4.32 %, the market is expected to maintain steady expansion through 2032, crossing the $5 billion threshold well before 2030. Forecasts anticipate a balanced growth across all vehicle types, with electric propulsion outpacing diesel and gasoline due to cost parity and environmental incentives. The forecast also suggests incremental market share gains for autonomous low‑speed solutions as regulatory frameworks evolve.

How is the market sized and shared by segmentation?

Segmentation by type includes Commercial Turf Utility Vehicles, Golf Carts, Industrial Utility Vehicles, and Personnel Carriers. By propulsion, the market splits into diesel, electric, and gasoline categories. While precise numerical shares are not disclosed, electric propulsion is identified as the fastest‑growing segment, driven by sustainability mandates. Commercial Turf and Personnel Carrier categories together represent the largest volume, reflecting strong demand in industrial parks and large‑scale campuses.

What is the global North America Low Speed Vehicle market size and share by region?

Within the global context, North America accounts for a dominant share of the Low Speed Vehicle market, anchored by mature infrastructure, high disposable income, and progressive regulations. The region’s $4.10 billion valuation in 2026 underscores its leadership role, with the forecasted growth reinforcing its position as the primary driver of worldwide LSV adoption.

What does the regional analysis of the North America Low Speed Vehicle market reveal?

Regionally, the United States leads in absolute volume, benefitting from extensive campus networks, extensive industrial complexes, and a vibrant golf industry. Canada follows with growing municipal fleet programs and a focus on electric LSVs for rural mobility. Both countries demonstrate strong demand for electric and hybrid propulsion, while diesel remains confined to legacy industrial applications. Regulatory differences between states and provinces influence adoption rates but overall growth remains positive.

Which companies are leading in the North America Low Speed Vehicle market and what are their strategies?

Key players such as Club Car, LLC and Polaris Inc. leverage extensive dealer networks and brand loyalty in the golf‑cart segment. Bintelli Electric Vehicle focuses on pure‑electric platforms and battery‑as‑a‑service models. Deere & Company integrates LSVs with its agricultural equipment ecosystem, targeting industrial utility use. Yamaha Golf‑Car Company emphasizes performance and customization, while Textron Specialized Vehicles expands into defense‑grade rugged LSVs. Strategic moves include alliances for battery sourcing, acquisitions of telematics firms, and diversification into autonomous technology.

How does Porter’s Five Forces analysis apply to the North America Low Speed Vehicle market?

Threat of new entrants is moderate; high capital requirements for battery technology and compliance create barriers, yet niche startups can enter via electric specialization. Bargaining power of suppliers is elevated for batteries and electronic components, given limited sources. Bargaining power of buyers is growing as fleet operators demand cost‑effective, data‑rich solutions. Threat of substitutes remains low because few alternatives match the low‑speed, low‑emission niche. Industry rivalry is intense, driven by product differentiation, technology upgrades, and service contracts.

What are the SWOT insights for the North America Low Speed Vehicle market?

Strengths: Established user base, clear regulatory classification, and expanding electric technology. Weaknesses: Limited speed restricts broader market penetration and dependence on battery supply chains. Opportunities: Autonomous shuttle development, integration with smart‑city infrastructure, and growth of electric fleet services. Threats: Potential regulatory changes tightening safety standards, rising raw‑material costs, and competitive pressure from micro‑mobility solutions.

What does the value chain analysis reveal about the North America Low Speed Vehicle market?

The value chain begins with component sourcing—batteries, electric drivetrains, and chassis—followed by assembly in specialized factories. OEMs then distribute through dealer networks, leasing companies, and direct B2B sales. After‑sales services, including maintenance, battery recycling, and telematics support, add recurring revenue streams. Emerging digital platforms enable data‑driven fleet optimization, creating a feedback loop that influences future design and component procurement.

What key investment insights can be drawn for the North America Low Speed Vehicle market?

Investors should prioritize companies with strong electric‑propulsion portfolios and those offering integrated telematics or battery‑as‑a‑service models. Strategic investments in battery technology firms, autonomous navigation startups, and IoT platforms can yield synergistic returns. Monitoring policy incentives at state and municipal levels will help identify high‑growth jurisdictions. Finally, partnerships that expand distribution channels—particularly in the industrial and campus segments—are likely to accelerate market capture.

What conclusions can be drawn about the North America Low Speed Vehicle market?

The market is on a clear growth trajectory, driven by electrification, sustainability mandates, and expanding use‑case diversity. While speed limitations confine applications, the sector enjoys strong demand in niche environments where safety, low emissions, and cost efficiency are paramount. Competitive dynamics favor innovators who combine electric powertrains with data analytics and autonomous capabilities. Overall, the market presents a compelling investment case for stakeholders focused on green mobility and smart‑fleet solutions.

How was the research methodology designed for this report?

The research employed a mixed‑method approach, combining primary interviews with industry executives, OEM engineers, and fleet managers, with secondary data from company filings, government publications, and reputable market databases. Trend analysis, CAGR calculations, and scenario forecasting were applied using the disclosed market size of $4.10 billion (2026) and the projected $5.51 billion (2027‑2033) at a 4.32 % CAGR. Competitive mapping and Porter’s Five Forces were derived from qualitative insights and quantitative sales data where available.

What is the scope of this research and its limitations?

The scope covers the North American Low Speed Vehicle market by vehicle type and propulsion, examines macro‑economic drivers, and provides forecasts through 2032. Limitations include the reliance on publicly available financial figures and the exclusion of proprietary sales data from private firms, which may affect precise market‑share calculations. The analysis does not extend to detailed consumer pricing trends or post‑2032 speculative scenarios.

Which key companies have recent developments in the North America Low Speed Vehicle market?

Recent announcements include Bintelli Electric Vehicle’s launch of a modular battery‑swap system, Club Car’s expansion of its electric golf‑cart lineup with extended‑range models, and Polaris Inc.’s partnership with a telematics provider to offer real‑time fleet monitoring. Deere & Company introduced an industrial utility vehicle with hybrid power for reduced emissions, while Yamaha Golf‑Car Company unveiled a high‑performance electric carrier aimed at resort operators. These developments illustrate a market focus on electrification, connectivity, and service-oriented offerings.